“Why can’t I save money? I should be able to do it…”

Do you find yourself asking that question a lot?

You make a decent salary, many others would be happy getting paid as much as you. Maybe you have a few debts, but nothing that’s not manageable.

So why can’t you seem to put any amount into savings? You know something needs to change.

But don’t be discouraged! Many people are in your situation. Whatever your salary, you can save some of it.

Let’s take a look at some reasons why you can’t save money along with solutions:

1. You were never taught how to save money

We’re not generally born with good money sense. This is something that has to be taught and practiced. If you were never taught how to save money beginning at a young age, it’s quite possible you still don’t know how to save money as an adult.

Solution: The good news is that you can still learn how to save money! You can do this by reading helpful articles, tracking your spending, and implementing smart money habits with the tips you learn.

2. You are an impulse spender

Spending money is fun. I get that, I really get that. There are studies out there that prove that shopping can be therapeutic. But did you know that dopamine (the feel-good hormone), is actually released before you make a purchase? It begins before the purchase happens. You don’t even have to make a purchase to get that good feeling. If you find yourself making impulse purchases to make yourself feel better, this could be a reason why you can’t save money.

Solution: Just browsing or window shopping can positively impact your mood and release dopamine. If you find yourself making many impulse purchases, take 48 hours, a week or even 30 days to think about a non-essential purchase. You might be surprised to discover that you don’t actually need that item and feel content leaving it at the store.

3. You don’t track your spending

A big reason why you can’t save money might be because you aren’t tracking what you spend. When you track your spending, you can track overspending and you can eliminate wasteful spending habits. This is also a great way to discover you are paying for a subscription that you no longer use.

Solution: Use a notebook or a simple app to write down your expenditures. You might also find the idea of a Spending Journal perfect.

4. You don’t use cash

One possible reason why you can’t save money might be because you aren’t using enough cash. You mostly swipe that credit or debit card. I know when I have cash in my wallet, I think harder about any purchases I want to make. I often decide I don’t need something when I think of the bills leaving my wallet.

Solution: Start using cash. This doesn’t mean you need to use cash for every single thing. (there can be benefits to using credit cards.) But perhaps you can try using cash for your clothing or entertainment budget. I have a set of printable cash envelopes and spending trackers that might be useful too.

5. You are dealing with lifestyle inflation

Lifestyle inflation or lifestyle creep is when your expenses increase along with any increase to your income. Maybe you think every time you get a raise or receive a promotion, you deserve to treat yourself with something new. For example, with your increase in income, you might think a new car is a good idea. But really, this just means the more you earn, the more you spend.

Solution: Take the time to learn contentment. If all of your basic necessities and bills are taken care of, with any increase to your income set up automatic deposits to your savings account with the difference. You should start seeing a healthy savings account grow!

6. You think you need something you want

A house is something you need and a car is something you need to get to work. (Although, we often overspend on this necessity because we want a certain vehicle, when we can simply focus on one that we need. Which is any reliable vehicle, really.) A fridge is something you need but a 65′ TV is something you want. Not knowing the difference between and need and a want can be the reason why you can’t save money.

Solution: Take a hard look at your thought process when it comes to purchases. Is it something you need or is it something that you want? If it’s something you want, start saving your dollars so you can purchase it guilt free.

7. Everyday expenses are rising (inflation)

As I’m sure you are aware, we are seeing big price inflations on pretty much everything these days. Housing, groceries, gas… While you can’t stop it, there are things you can do to alleviate the pressure on our wallets. (I like this article on the causes of inflation, if you’re interested to read more.)

Solution: Think of this as an opportunity to be creative. Think about ways you can create more income. Or trade your garden vegetables for fresh eggs from your neighbor. Go through your expenses with a fine tooth comb to weed out the expenses that are not 100% necessary in this season. Consider eating more vegetarian meals. Brainstorm to get your creative ideas going.

8. You don’t have a savings goal

Having a savings goal in place for something specific can be a great motivator. When you are just putting money into the bank for the sake of putting money into the bank on a regular basis, it can be easier to withdraw for unimportant reasons. When you implement a savings goal, you are more likely to save more money. It helps to create healthy and productive money habits.

Solution: Implement a savings goal. An emergency fund is a common, but great savings goal to start with. Once you’ve established your emergency fund, you can move onto paying off a debt. Then you can keep going with something else. Like a vacation fund, or new appliance fund, or a new to you car fund. With a goal in place, you’ll start to see how every money decision impacts your greater financial health.

One thing is for sure though, if you’re struggling to save money, you’re not alone. With the help of these 8 solutions, you’ll be well on your way to reaching your savings goals. Which of the 8 reasons do you resonate most with?

Spending money is fun, but saving money can be fun too! It’s fun to pay cash for the things you saved for!

Who doesn’t love going on vacations? Or buying a new TV? Or whatever is on your wish list? It’s even more fun when you can enjoy those things without a guilty conscious because they’ve already been paid for.

We all know how tough it is to pinch a penny these days. Saving money isn’t easy, but with a little creativity and some willpower, you can save between $2,000 and $5,000 a year with a few simple tips and hacks. So here’s how to save $2,000 – $5,000 (or more!) a year.

Start Off by Setting a Goal

In order to save $5,000 a year, you’re going to have to set aside about $417 a month. But if this amount is making your heart race, (don’t worry, it sounds scary to me too) then try saving $2,000 a year. You’d only have to set aside about $167 a month to reach your goal.

Cut down on takeout

No, you don’t have to let go of your takeout cravings completely. But consider cutting down 80% on takeout food. If you’re not tracking your expenses, you probably don’t realize just how much money you’re throwing away at on takeout.

But for example, if you order the Big Mac meal for $10 once a week, (just once!) that’s $40 a month. If you cut down this vice out of your annual expenses, you would’ve managed to save $480 a year.

Don’t Pay for Netflix

Say goodbye to your Netflix subscription. Or Disney+. Or Spotify.

Think about any monthly subscriptions that you have and consider cancelling one or two for a little while.

The cost for Netflix’s standard plan is about $15.49 a month. That’s $185.88 a year you could save if you forego this popular streaming service.

Think about the savings you will see if you cancel more than one service.

This can also become a fun exercise in creativity when you need to fill your downtime with something entertaining.

Start a $5 jar

Have you heard of the $5 jar hack before? How it works is, every time you find yourself with a $5 bill, you put it in a jar. Simple, right?

You’ll find that all those $5 bills really add up quickly and painlessly!

Save Your Raise

Say you got yourself a raise that will give you $2,000 a year after taxes. The simplest way to save is to pretend like you never got the raise in the first place. (Only if you can manage it with the cost of living these days!)

So, every month, transfer $167 into your savings account and in a year you’ll have $2,000 to play with!

Cut Down on Starbucks

The average price of a Starbucks tall latte in Canada is $3.85. If you go to your local Starbucks five days a week, you’re spending $19.25 a week, $77 a month, and $924 a year on average.

But if you cut down on Starbucks or drive-thru coffee in general and settle for the coffee in the break room or from home, you could save yourself nearly $1,000 a year.

Try your hand at DIY oil changes

If you are an ambitious type and enjoy a challenge, doing your own oil changes at home can save you a lot.

Learning how to drain and replace the oil and other fluids is easy. There are tons of online tutorials on YouTube that can teach you how to do it.

Same with changing your tires from summer to winter tires and vice versa. Save yourself a good chunk of change by learning how to do these yourself.

Reduce your carbon footprint

The average person spends about $386 per month on gas for their car. That’s $4,632 a year.

You can reduce your monthly gas expenses by carpooling, using public transportation like the subway or a bus.

If all else fails, try walking or riding a bike. It’s healthy and 100% free.

Sign up for PC Optimum

PC Optimum is a points program that is available at Real Canadian Superstore, Shoppers Drug Mart, or other Loblaw banner stores.

You collect points on your purchases, which can then be redeemed in $10 increments off any purchase you make at these stores.

The average cost of a gym membership is about $50 a month. That’s $600 a year, and if you add the initiation fee, it will probably be more like $800.

Consider canceling your membership and go for a nice jog around the block or do some push-ups at home. There are tons of YouTube channels with 40, 50, and 60-minute workouts that are just as good.

Reduce Your Cell Phone Plan

All those Smartphone data plans you got suckered into getting could run you at least $80 a month. That’s $960 a year on average.

But you can find carriers that offer prepaid data plans. If you run out of credit, just use Wi-Fi and let people know they can only reach you when you find free Wi-Fi. This will help you save about $480 a year.

All in all, just shop around to find something that will suit your needs at the lowest price.

Get a Part Time Job

Sometimes, the best way to save $2,000 to $5,000 is to earn it.

The average minimum wage in Canada is $15.55 per hour. So, if you work 15 hours a week, you’ll earn about $233.25. That’s $933 a month and $11,196 a year, minus the taxes.

As you can see, eliminating little things here and there can really add up! Try adopting a few of these ‘how to save’ techniques, even for a short time and see how much you can save!

I’d love to hear all your ideas for how to save $2,000 – $5,000 a year. Drop a comment below!

The biggest shopping day of the year is about to happen in a few weeks. I’m pretty sure it now rivals and perhaps beats out Boxing Day sales in Canada. Black Friday can be a fantastic time to score great deals on Christmas gifts. It can especially be a great time to shop if you know a few tips and tricks to make your shopping successful.

Here are 9 useful Black Friday shopping tips:

Bookmark my giant Black Friday post

Coming up next week, I will have my annual list (it’s giant!) of Canadian Black Friday deals. Simply peruse the list to find the stores that interest you, click the links, then start shopping from the comfort of your own home!

Buy discounted cards for the stores you will be shopping at.

Go shopping with discounted gift cards instead of cash to save yourself some moolah! There are many stores like Real Canadian Superstore/Loblaws, Rexall and Shoppers Drug Mart that offer discounts on gift cards for stores such as Old Navy and Gap during their weekly sales. You might also want to take a look at CardSwap.ca for discounted gift cards.

Ditch the big shopping cart if you’re shopping in-store.

Just don’t even think about getting one of those large cumbersome shopping carts if you plan on shopping in-store. Grab a basket or bring a large reusable shopping bag (IKEA bag anyone?) to avoid collisions or getting stuck in an aisle when you just want to get in and out of the store as quickly as possible.

Make your shopping list in order of importance.

Is Santa promising to bring a Lego set this year? You better put that first on your shopping list! By making your shopping list in order of importance, you’re really helping yourself to not forget that all important gift.

Sign up for emails for the stores you will be shopping at.

Whether you’re shopping in-store or online it can be extremely valuable to sign up for the email list of the stores you will be shopping at. Almost certainly, they will include coupon codes or coupons you can print/show on your phone for an extra discount. Often times email subscribers can also start shopping the sales earlier online.

Shop online.

The same sales are typically available online too, save for the extreme doorbusters. Save yourself some time and energy by shopping from the comfort of your own home. (This is my preferred method ;))

Join loyalty programs

Might as well join the loyalty programs for the stores you will be shopping at if you haven’t already! Collect points that can translate into free items or even extend certain perks. (I’m thinking the TJX card from Winners.)

Shop online at Amazon.

Because I’m such a fan of online shopping, I usually check Amazonfirst. Black Friday will be no different because I find that they usually have some great one day deals. Another Amazon tip: Use Honeyto track Amazon prices so you can see how today’s Amazon price compares to the last 30 days. You can even use the Droplist feature which allows you to save items you’re interested in and once Honeydetects a lower price, they’ll let you know.

Set a budget and stick to it.

You’re really not getting any deals per say, if you put yourself into debt trying to get the latest and greatest thing. If you’ve created a shopping list, it should be easy to stay within budget because you have an idea of the price of each item. Don’t ruin your holidays worrying about debt! There’s rarely any deal that is worth that amount of stress.

Do you shop on Black Friday? I’d love to hear your Black Friday Shopping tips in the comments below.

Simple ways to celebrate the holidays on a tight budget

For some of us, the holidays always seem to land during a time where everything else hits. This means a tight budget during the holidays is a common issue that most of us will face at some point in our lives. If you find yourself with a tight budget this holiday season don’t let it ruin your fun.

This year, learn how to rock the holidays on a tight budget with these simple but meaningful ideas.

Focus on Meaning

Focus on the meaning of the holidays instead of the frills and trappings. The holidays are about friends and family so focus more on making memories than having a fancy holiday. Make homemade decorations, bake cookies, and spend quality time with the people you love.

Create new traditions

It’s the perfect time to create new traditions that your family will remember for years to come! Here are some ideas that you may enjoy or get you brainstorming:

Go on a Christmas tree hunt: Growing up, my favourite tradition was going into the forest (with our free permit to cut a tree) and searching for the most perfect tree to decorate.

Decorate on December 1st: Another thing we would do is wait until December 1st to decorate the house. December 1st also meant we could crank the Christmas carols!

Make homemade Christmas cards: This would be a super fun afternoon activity for the whole family!

Give to the less fortunate: I know locally, there are several businesses that set up bins to collect toys. Perhaps, you could find something similar and team up with a few friends to help take the focus off of yourself.

Decorate a Gingerbread house: This is always a fun activity for the kids! Or decorating sugar cookies is also fun!

Write letters to Santa: Sit down with the kids and write letters to Santa! Don’t forget to send them off! In Canada, you can send your letters to:Santa Claus North Pole HOH OHO Canada

Read a Christmas book every day in December: Head to your library and pick up a big stack of holiday books to read together.

Have a Christmas movie night: One for the whole family and maybe one just for mom & dad!

Seek out the best Christmas light display: Take a drive one night just to look at all the lights. Vote for your favourite display.

Give Christmas PJ’s on Christmas eve: For the last few years, I have been wrapping up a pair of Christmas pajamas for both girls that I got on sale and giving it to them on Christmas eve. They love to wake up Christmas morning in their new Christmas pajamas!

Make Homemade Gifts

Save money but still enjoy the gifting part of the holidays with Homemade Christmas gifts. Use the things you have on hand to make personalized, meaningful gifts for the people you love. It’s the fact that you thought of them and wanted to do something special that makes gifts so wonderful. Baking homemade gifts is a great way to use items you have on hand to create a great gift someone will appreciate.

Earn Extra Cash

A great way to deal with a tight budget during the holidays is to work on simple ways to earn extra cash. Sell off things you do not need or crafts you have made that others can give as gifts. Cleaning houses and clearing snow are both great ways to earn extra cash as the season wears on. This is the best time of year to pick up a part-time seasonal job for extra money if you have the time to spare.

Make a Holiday Budget

To help you thrive during any time with a tight budget, create and stick to a budget. This is a plan to help your family stay on track financially. Plan all of your regular expenses first so you don’t end up making your situation worse for the sake of the holidays. This will leave you with a clear idea of how much you can really spare and how much you should try to earn instead of going ahead blindly.

Look for Free Activities

Look for free fun activities to do. You can still make the most of Christmas even when you can not afford much. Go for a stroll and check out neighborhood light displays, volunteer to help others down at the soup kitchen or food bank. Find reasons to be grateful for what you do have this season, and you will be well on your way to rocking the holidays on a tight budget!

What are your best tips for making a meaningful but frugal Christmas season?

Many years ago I embarked on my very first no spend challenge. This is when I spent zero dollars for a whole 30 days. That’s right…zero spending for an entire month! (except for bills and a few groceries.)

When I embarked on my first no spend challenge, I just jumped right in without a plan. I will tell you that I was successful in completing the challenge, however, it could have been so much smoother if I had a plan in place!

“If you fail to plan, you are planning to fail,” quoted by Benjamin Franklin, is excellent advice to put in place when you are embarking on a challenge of not spending a dime for 30 days.

The thought of no spending for a month is downright daunting… but then to face the challenge without any plan in place?! We all know that we can pretty much expect defeat.

That is not what we want.

So, today, I’m going to outline several ways to plan for a successful no spend challenge.

But first…

Why do a No Spend Challenge?

Not spending any extra money for 30 days can sound crazy, I know. However, a No Spend Challenge is a great way to reset our spending habits.

The end goal for me personally, is not to deprive myself, but to reframe how I spend money.

Completing a No Spend Challenge helps me to make more intentional purchases that align more with my true financial goals.

Speaking of goals, a no spend challenge is also a great way to kickstart your financial goals.

Once you reset or reframe your spending habits to serve you, you will be well on your way to completing those goals you never thought possible!

Let’s plan shall we?

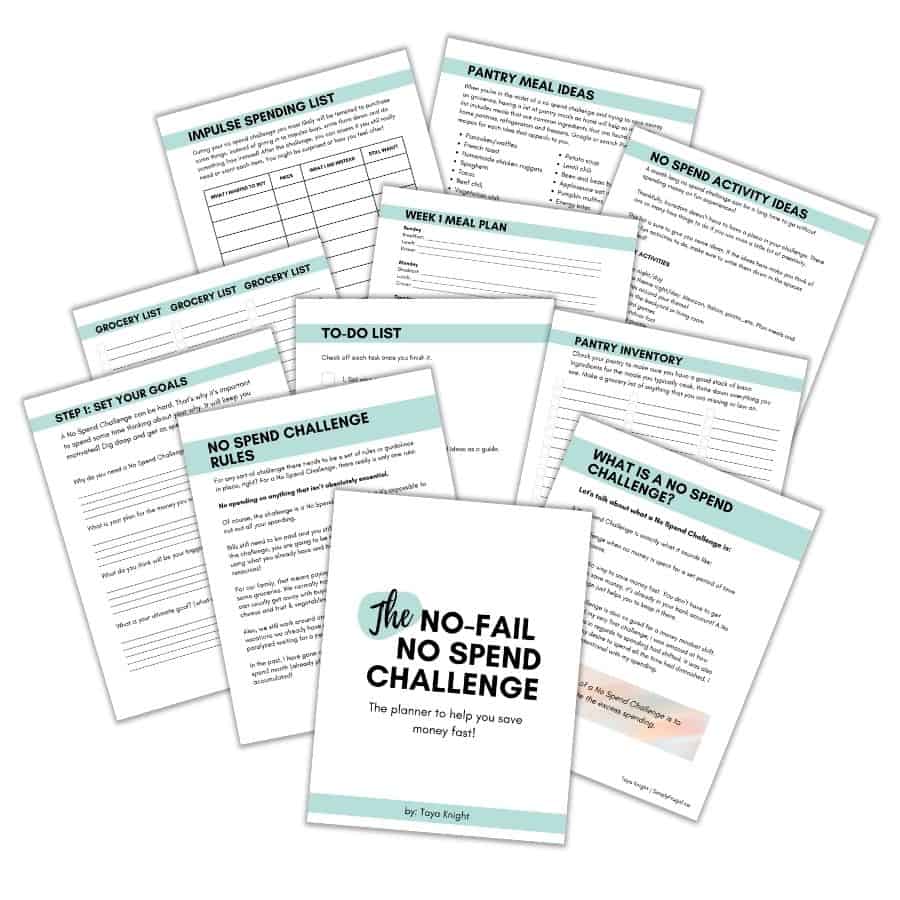

If you’re really looking for an in-depth system for a successful no spend challenge, I recommend my No Spend Challenge Planner! It’s 45 pages of instructions, no spend activity ideas, pantry meal ideas, before and after challenge questions, food inventory sheets, gratitude sheets and so much more! Take a look here!

Step 1: Determine the length

The first step is to determine the length that your no spend challenge will last. If this is your first no spend challenge, I suggest starting small. Maybe a weekend, a work week or 7 days. Starting small will pretty much ensure a successful no spend challenge.

As you start to see the fruits of your no spend challenge, you can increase the frequency of your weekend/work week/7 day challenges. Or you can jump into a 30 day challenge to see the greatest increase in your savings account.

Step 2: Look ahead to what’s coming

Grab your calendar and take note of any events, birthdays or vacations you have coming up. You can either pick a period of time that avoids those events, or work around them.

I personally like to work around any events, birthdays, anniversaries, or family vacations we already have planned. This is so we don’t become paralyzed waiting for a perfect month. After all, any month or day is a great day to save money!

I should note that it’s possible to use creativity with planned events. In the past, I have gone on a quick vacation to Vancouver during a no spend month (already planned) and used only gift cards that I had accumulated!

Step 3: Take Inventory

This is a crucial step to having a successful no spend challenge.

Before I embark on a no spend challenge, I take inventory of my fridge, pantry, freezer and anywhere I keep household supplies.

I mark down everything I find. I’m often surprised at what I do find. Lol. Sometimes I have no idea that there are two pork tenderloins frozen in the freezer, for example.

During a typical month, food can be a huge area of the budget. By taking inventory for a no spend challenge, you will greatly reduce the amount of money you need to spend on food because you can use what you already have on hand.

This is a great time to quickly jot down some meals that you can make with the ingredients that you find.

Step 4: Use creativity

One of the hardest parts of a no spend challenge can be figuring out how to use what you have or learning to go without. This is where a bit of creativity can really pay off!

Here are some ideas to get your creativity flowing:

Trade your abundance with friends (have a lot of zucchini but need toiletries?).

Take to Pinterest to be inspired with meal ideas or simple DIY projects to create things with stuff you already have.

Save money by buying just one of something instead of 10.

Shop only where you have gift cards.

Order any groceries you need online so you aren’t tempted to impulse buy.

Borrow a book, audiobook or video from your library.

Take advantage of free community events .

Carpool to work.

Declutter and sell items to make some cash.

Go on a walk with a friends instead of going for coffee.

A no spend challenge can be a real eye opener on how you really spend your money on a normal basis.

During a challenge, this is a great time to assess where you really value spending money. On the other hand, you can also assess what you are wasting money on without even realizing it.

Instead of spending money all the time as a solution, a no spend challenge will help you to work with what you already have. So needs may become wants as you work through creative solutions.

I have no doubt that a successful no spend challenge will teach you lessons that will last a lifetime.

How to do life after your challenge

Immediately after a no spend challenge is an important period.

You don’t want to fall back into any bad spending habitsor go on a shopping spree to make up for days without spending anything.

This is a good time to look at how much money you saved during your no spend period as well.

What do you plan to do with your savings? Are you going to transfer it to your savings account or use the extra money to pay some bills or debt?

After you decide what you’re going to do, take action immediately. Put the money to use right away, or you might be tempted to use it for the wrong thing.

One last thing. Remind yourself constantly of what you really want your money to do for you. Do you want to pay off your mortgage as quickly as possible? Do you want to spend a month traveling Europe? What ever your true financial goals are, write them down and keep them in a visible spot so you’re constantly reminded. Don’t shortchange yourself. You are worth it.

This was such a big hit in past years, that I took the time to update it with this year’s dates! Hope you enjoy 🙂

Are you living in the Okanagan or planning on taking a trip there this summer? The Okanagan happens to be the place I call home, so I thought I’d create a guide full of fun, frugal activities that take place in the land of sun. The goal is for this to be The Ultimate Frugal Okanagan Summer Activity Guide. If you have an event or know of a really cool place to visit, let me know and I’ll add it to the list!

Grouponhas a ton of local discounted restaurants, spas, things to do and more! Check it out for great savings on the things you want to do in the Okanagan.